Robotaxi Deployment

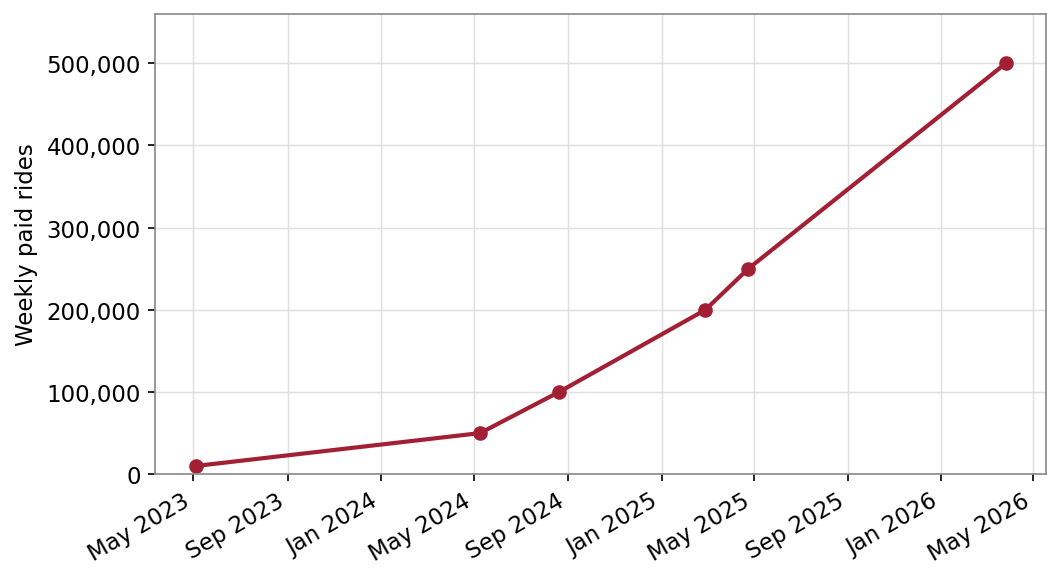

Waymo weekly paid robotaxi rides, disclosed milestones | Source: Waymo / Alphabet company disclosures.

Waymo’s weekly paid-ride count is the clearest single measure of robotaxi scaling. The disclosed milestone series runs from roughly 10,000 weekly rides in May 2023 to 500,000 by late March 2026, with the fleet reported at approximately 3,000 vehicles covering more than four million autonomous miles per week.[3]

Tesla’s footprint illustrates the recurring gap between announced coverage and deployed scale: its Q1 2026 SEC filing lists three Texas metros ramping unsupervised and five more in preparation, while third-party trackers put the active unsupervised Austin fleet at roughly two dozen vehicles.[4]

Robotaxis achieved significant scale during 2025. Waymo reported 500,000 paid rides per week across 10 U.S. metros by late March 2026, roughly a tenfold increase in under two years, against a stated year-end 2026 target of one million weekly rides.[1] Tesla robotaxis now provide unsupervised rides across Texas, and Zoox is now offering driverless rides in Las Vegas. All three have significant expansion plans for 2026 and beyond.

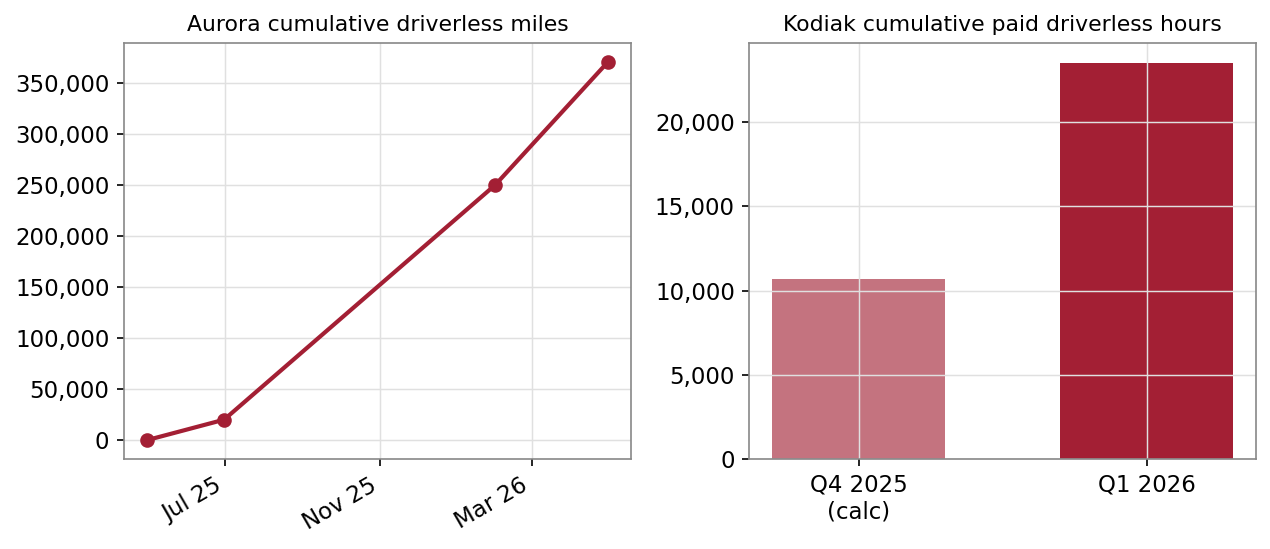

Autonomous trucking reached commercial driverless operation in 2025 but remains in the early stages of commercialization. The two public pure-plays, Aurora Innovation and Kodiak AI, together reported under $3 million in combined first-quarter 2026 revenue.[2] While the revenue remains small, Aurora has now stacked up more than 350,000 driverless miles and Kodiak logged almost 25,000 driverless hours in Q1 2026.

- Robotaxi ride volume is compounding fast; autonomous trucking is real but tiny in revenue terms.

- Every commercial U.S. deployment (both AV taxis and trucks) sits in Sun Belt states (TX, AZ, FL, GA, NV), driven by regulatory permissiveness and weather.

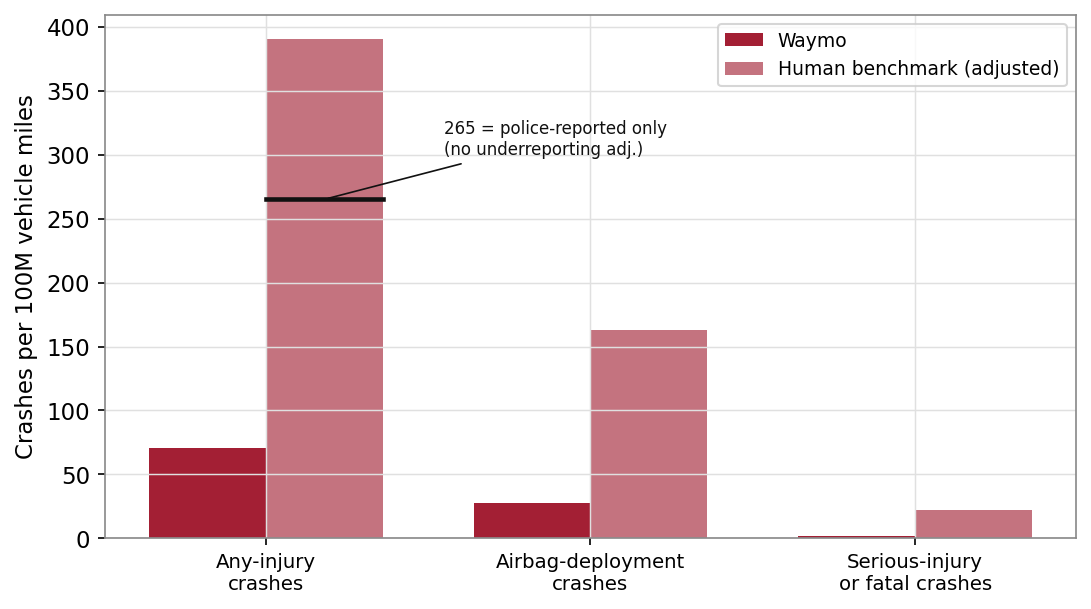

- On a benchmark-matched basis, Waymo reports materially lower crash rates than human drivers in the same cities; the comparison is operator-conducted and peer-reviewed, but not independently replicated.

- Announced coverage consistently runs ahead of deployed fleet size, most visibly for Tesla.

Autonomous Trucking

Aurora Innovation operates hub-to-hub on the Texas triangle (Dallas–Houston–El Paso–Phoenix); Kodiak AI operates primarily off-highway in the Permian Basin.

Autonomous trucking operating metrics | Sources: Aurora Innovation Q1 2026 Shareholder Letter and Kodiak AI Q1 2026 Results, both SEC 8-K Exhibit 99.1. Kodiak Q4 2025 hours derived from stated QoQ growth.

Safety

On a benchmark-matched basis, Waymo’s reported crash rates per 100 million vehicle miles sit far below the matched human benchmark across all three severity categories.

Crash rates per 100M vehicle miles, Waymo Rider-Only vs matched human benchmark, all locations, 170.7M driverless miles | Source: Waymo Safety Hub (incidents per million miles × 100). The 265 marker shows the any-injury human rate without the 32% underreporting correction.[6]

On 170.7 million fully driverless miles through December 2025, Waymo reports 92% fewer serious-injury-or-fatal crashes, 83% fewer airbag-deployment crashes, and 82% fewer any-injury crashes than matched human drivers.[5] The any-injury human benchmark includes a 32% upward correction for crashes that never reach police records; even without that correction, the human rate (265 per 100M VMT) remains far above Waymo’s (71). These are surface-street rates in Waymo’s operating cities, distinct from national figures, and the analysis is Waymo-conducted, peer-reviewed, but not independently replicated.

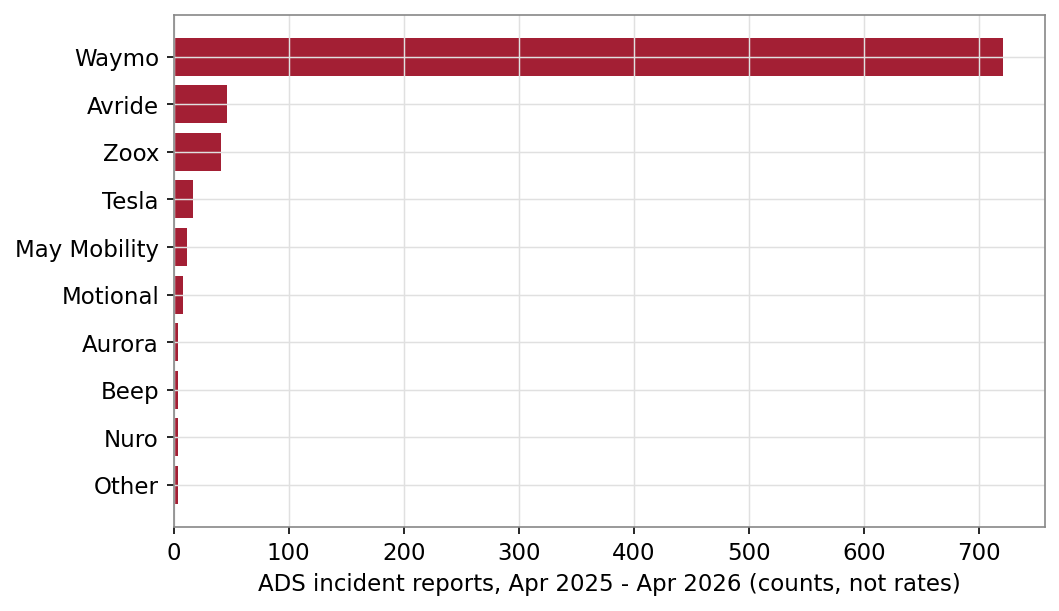

NHTSA Standing General Order ADS incident reports by entity, Apr 2025 – Apr 2026 (861 unique incidents) | Source: NHTSA SGO-2021-01. Counts, not rates: entities differ enormously in fleet size and miles driven.

Stated Company Targets

The figures below are company-stated forward targets from the sources noted, not independent forecasts.

What to Watch in 2026

- Whether Waymo approaches its one-million-weekly-ride target and lights up announced metros (DC, Las Vegas, Detroit) and first international markets.

- Tesla’s progress closing the gap between announced robotaxi coverage and deployed unsupervised fleet.

- Aurora’s path to 200+ driverless trucks and whether Q4 revenue delivers the back-half-weighted FY2026 guidance.

- Kodiak’s long-haul public-highway driverless launch, targeted for late 2026.

- Any NHTSA, CA DMV, or CPUC action that changes the regulatory cadence; whether independent researchers replicate the safety analyses.

Sources

[1] Waymo / Alphabet company disclosures (blog, X posts, executive interviews), 2023–2026. 500,000 weekly paid rides across 10 metros reported late March 2026; one-million-ride target stated by co-CEOs, Feb 2026. ↩

[2] Aurora Innovation Q1 2026 Shareholder Letter and Kodiak AI Q1 2026 Results, SEC 8-K Exhibit 99.1 (May 2026). Heavy and tractor-trailer driver employment per BLS OEWS. ↩

[3] Waymo Year in Review (Dec 2025) and co-CEO interview (Mar 2026): ~3,000 vehicles, >4M autonomous miles/week, 20M+ lifetime paid rides. Fleet count consistent with Waymo’s December 2025 report to NHTSA per press coverage. ↩

[4] Tesla Q1 2026 Update, SEC 8-K Exhibit 99.1 (Apr 22, 2026); Austin fleet estimate per third-party robotaxi trackers, flagged as non-primary in the workbook. ↩

[5] Waymo Safety Hub, “All Locations” incidents per million miles (verified June 2026); peer-reviewed companion: Kusano et al., Traffic Injury Prevention (2025). Underreporting correction per Blincoe et al. (2023), “The Economic and Societal Impact of Motor Vehicle Crashes, 2019 (Revised),” NHTSA Report DOT HS 813 403. National fatality context: NHTSA annual data (1.19 per 100M VMT, 2024). ↩

[6] The raw incident counts reported to NHTSA cannot be divided by miles and compared to human crash statistics. The Standing General Order captures essentially every contact event via telematics, while human benchmarks capture only police-reported crashes, which miss a large share of minor contacts. The valid comparison is benchmark-matched: same cities, same road types, with an underreporting correction applied to the human injury side. ↩

Companion workbook. technology-transportation-ai.xlsx: Robotaxi ride growth, deployment by metro, AV trucking metrics (Aurora & Kodiak), safety rate comparison, NHTSA ADS incident summary, driving occupations, company targets, CRE implications map