Demographics

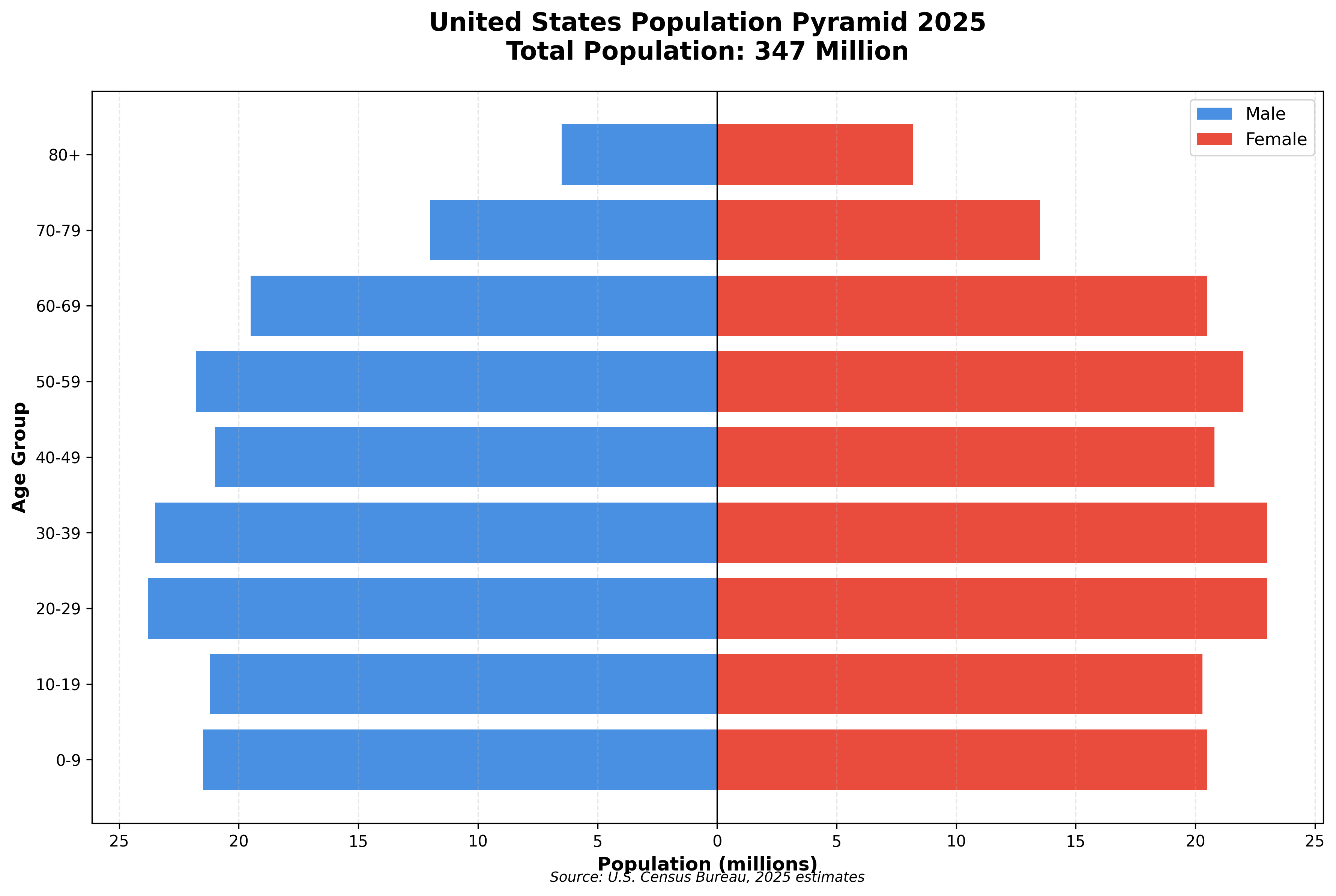

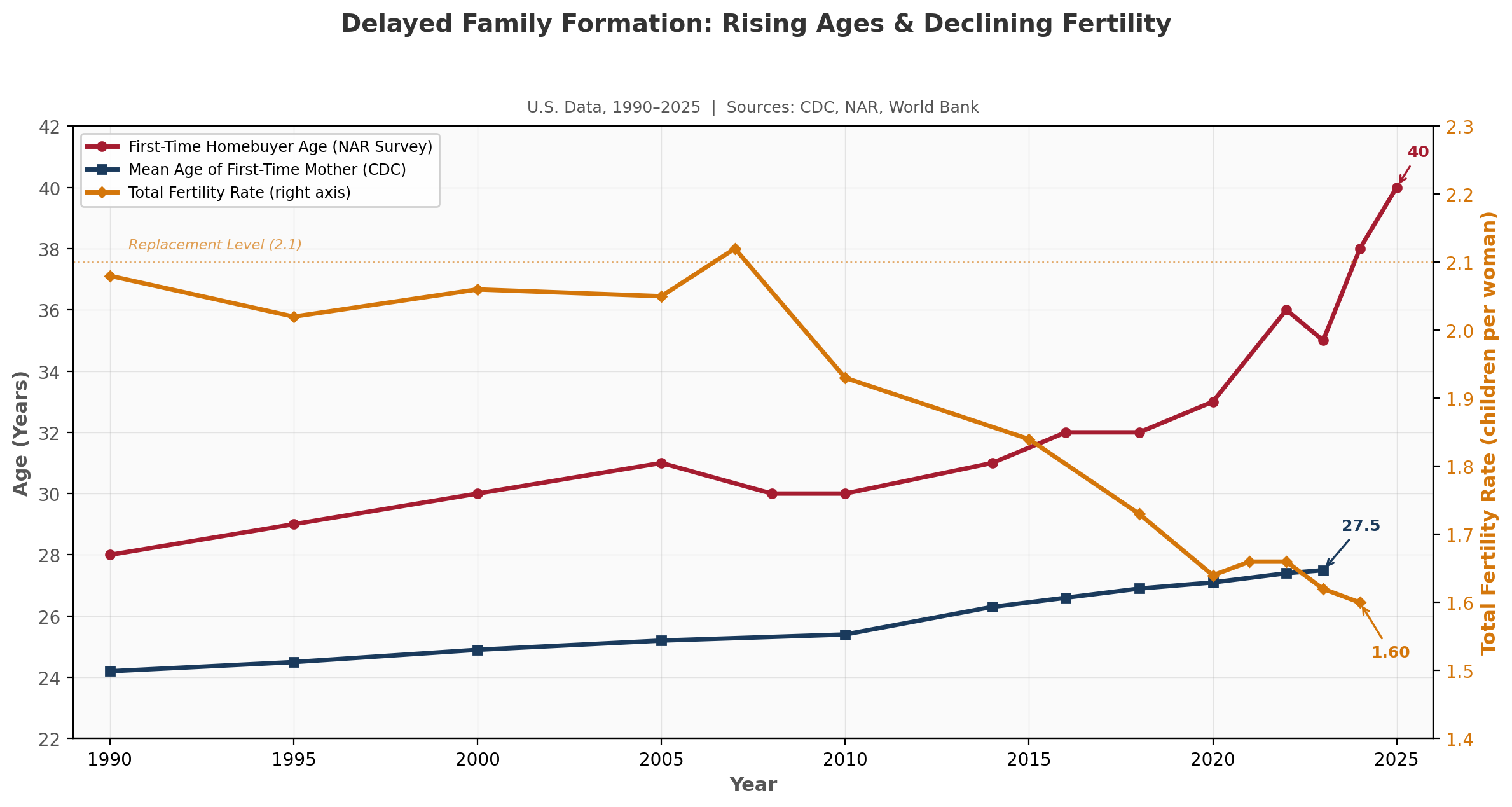

Millennials (age 29–44) and baby boomers (age 61–79) are currently the largest generations in the United States. As they graduate from entry level positions (millennials) and retire from the workforce (boomers), the much smaller Gen Z and Gen X cohorts are now filling those positions, contributing to nationwide labor shortages in industries including healthcare, construction, trucking, and logistics. This dynamic is even more pronounced in the rapidly aging nations of developed Europe and Asia, with China, Japan, and many Western European nations feeling the stress of top-heavy populations, placing additional burden on younger and smaller generations. The U.S. is increasingly following this demographic path, with reduced birthrates leading to delayed family formation and homeownership, and (more recently) reduced net immigration. This section summarizes and provides measurable context for demographic shifts currently in motion as respective generations change with the passage of time. As a CRE investor, demographics are key to understanding the evolving shape and texture of demand for multifamily/residential housing, senior living, office use, industrial distribution and manufacturing, and retail space.

Key Data Sources & Research

www.census.gov - Population estimates, American Housing Survey, migration data

www.cdc.gov - Birth rates, maternal age, mortality data

www.nar.realtor - Homebuyer profiles, market trends

fred.stlouisfed.org - Economic data, housing statistics

population.un.org - Global demographic forecasts

www.bls.gov - Labor force data, unemployment trends

ifr.org - Industrial robot density, global automation data