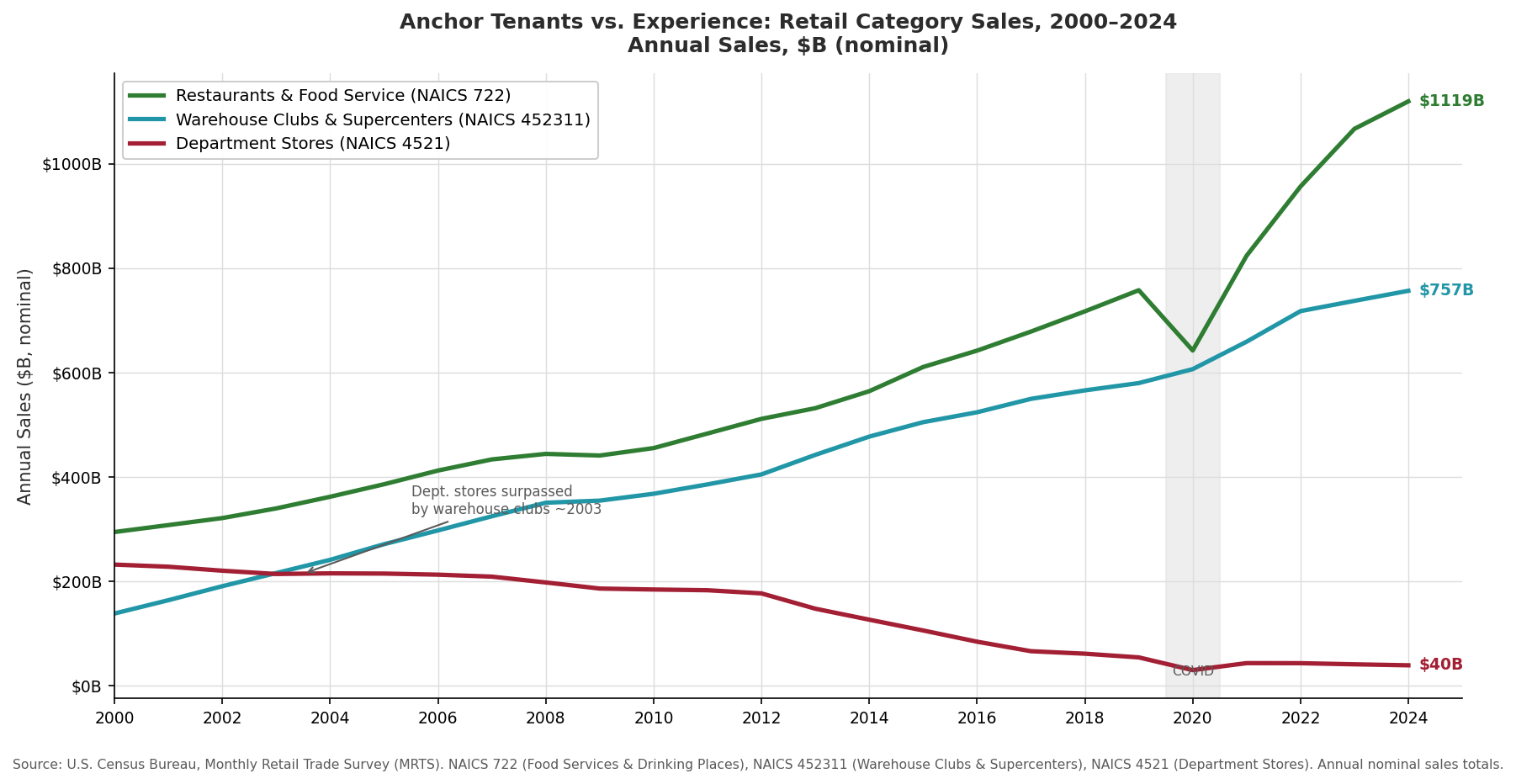

National retail vacancy statistics are frequently recorded in simple aggregate terms, combining at least seven distinct asset sub-classes* with distinct and often diverging fundamentals. These asset classes have evolved over 25 years of shifting consumer spending patterns, the rise of e-commerce, the contraction of department store chains, and the increasing dominance of food, beverage, and essential services as retail anchors. In one stark comparison of diverging success among retail asset types, department store annual sales have declined from $232 billion in 2000 to $40 billion in 2024, an 83% nominal decline over 24 years, while warehouse club and supercenter sales rose from $139 billion to $757 billion over the same period.[1]

* The seven formats covered in this page: enclosed malls, grocery-anchored neighborhood centers, unanchored strips, power centers, lifestyle centers, single-tenant/NNN, and urban/high street retail.

Charts

Retail Category Sales, 2000–2024

Department Stores, Warehouse Clubs & Supercenters, and Restaurants & Food Service: Annual Sales, $B (nominal) | Source: U.S. Census Bureau, Monthly Retail Trade Survey (MRTS) | Chart: CRE42

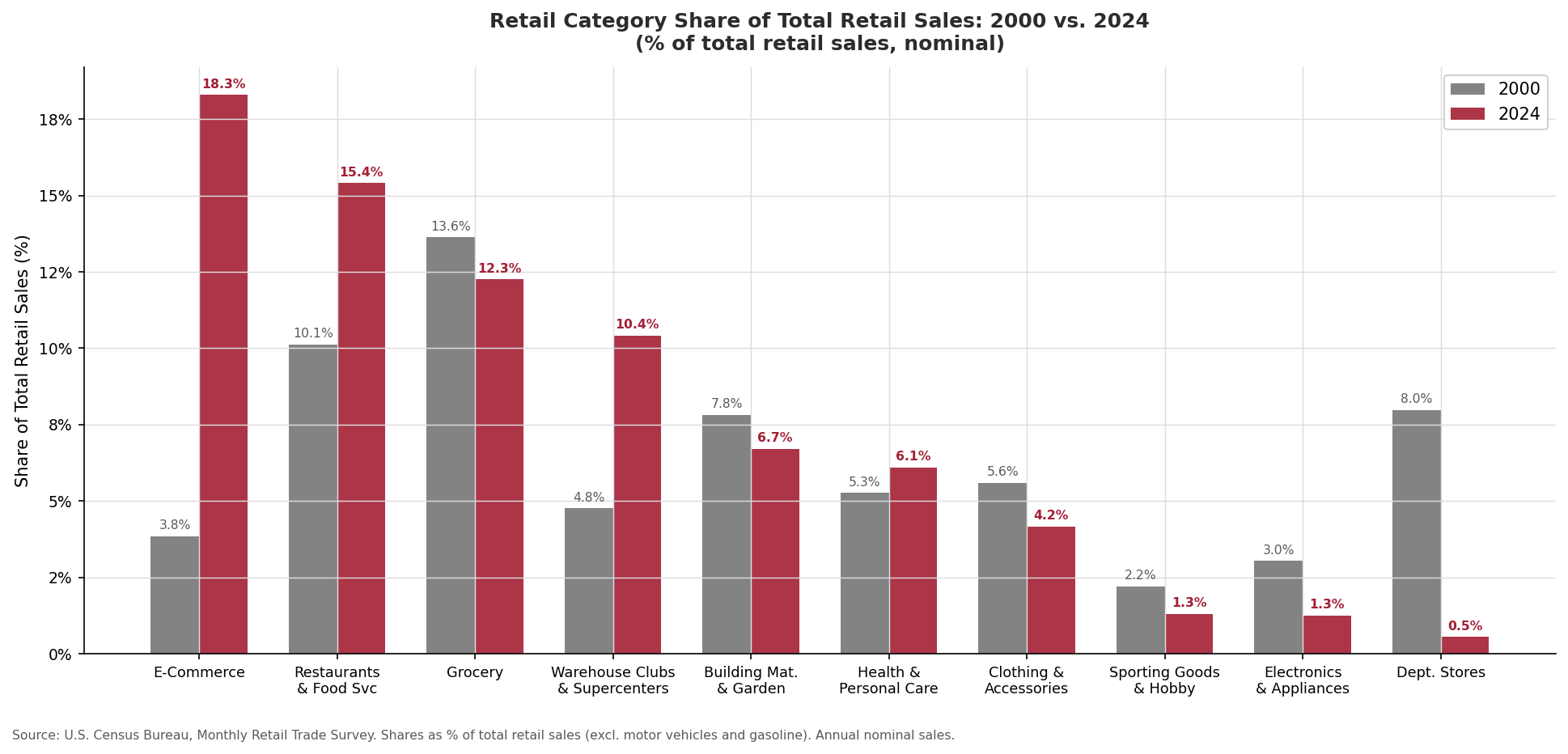

Share of Total Retail Sales: 2000 vs. 2024

Retail Category Share of Total Retail Sales: 2000 vs. 2024 (%) | Source: U.S. Census Bureau, Monthly Retail Trade Survey (MRTS) | Chart: CRE42

Key Observations (U.S. Census Bureau MRTS; Colliers, JLL, Cushman & Wakefield Q4 2025)

Context & Discussion

Single-Tenant / Net Lease

Single-tenant net lease (NNN) became an institutional asset class in the 1990s as national chains like McDonald’s, CVS, and Dollar General expanded aggressively and preferred sale-leaseback structures to free up capital. The NNN lease structure, under which the tenant pays property taxes, insurance, and maintenance, converts the landlord’s income stream into something resembling a corporate bond. This bond-proxy characteristic attracted income-focused REITs and 1031 exchange buyers, compressing cap rates to the tightest levels of any retail subtype.

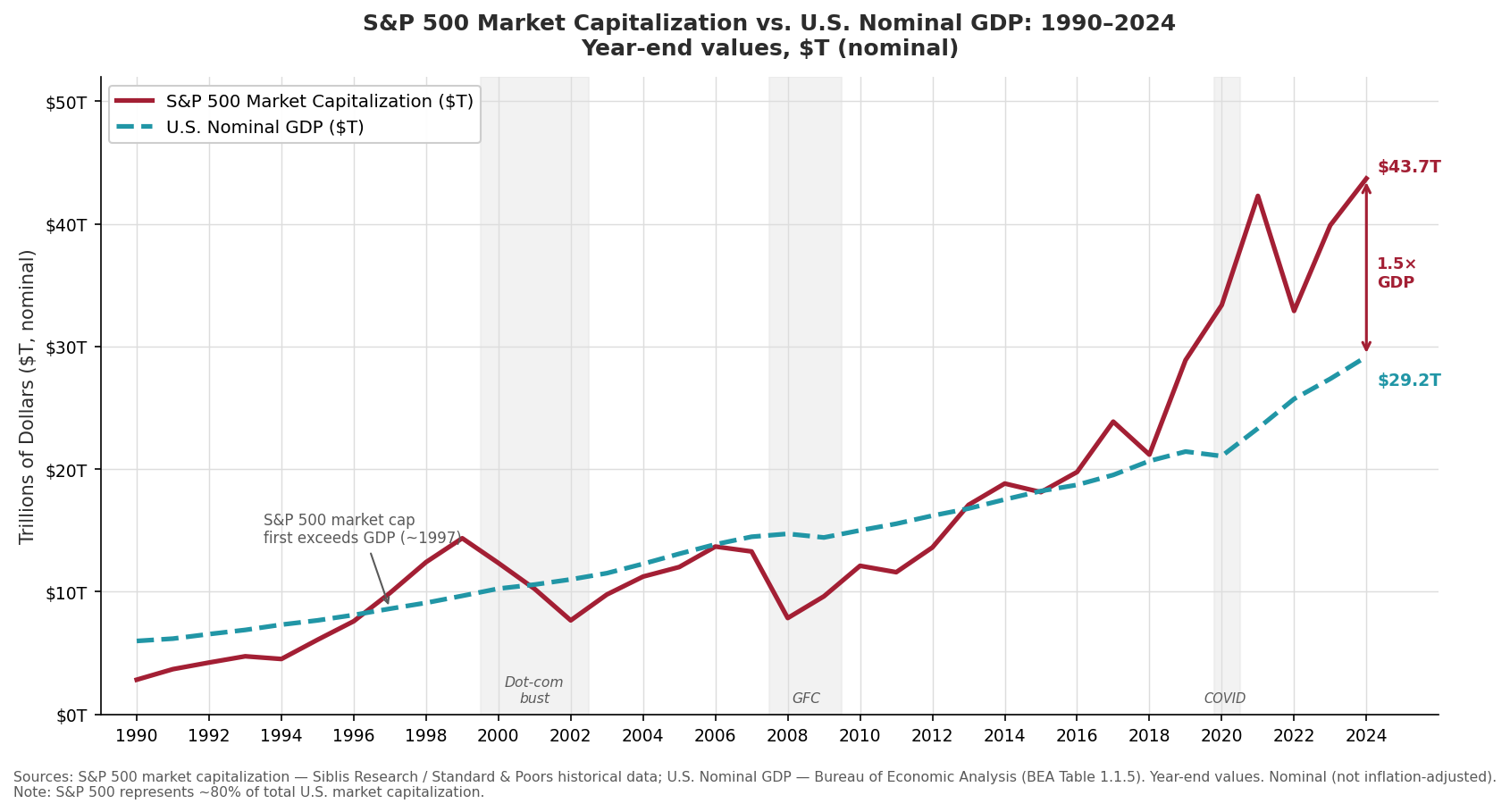

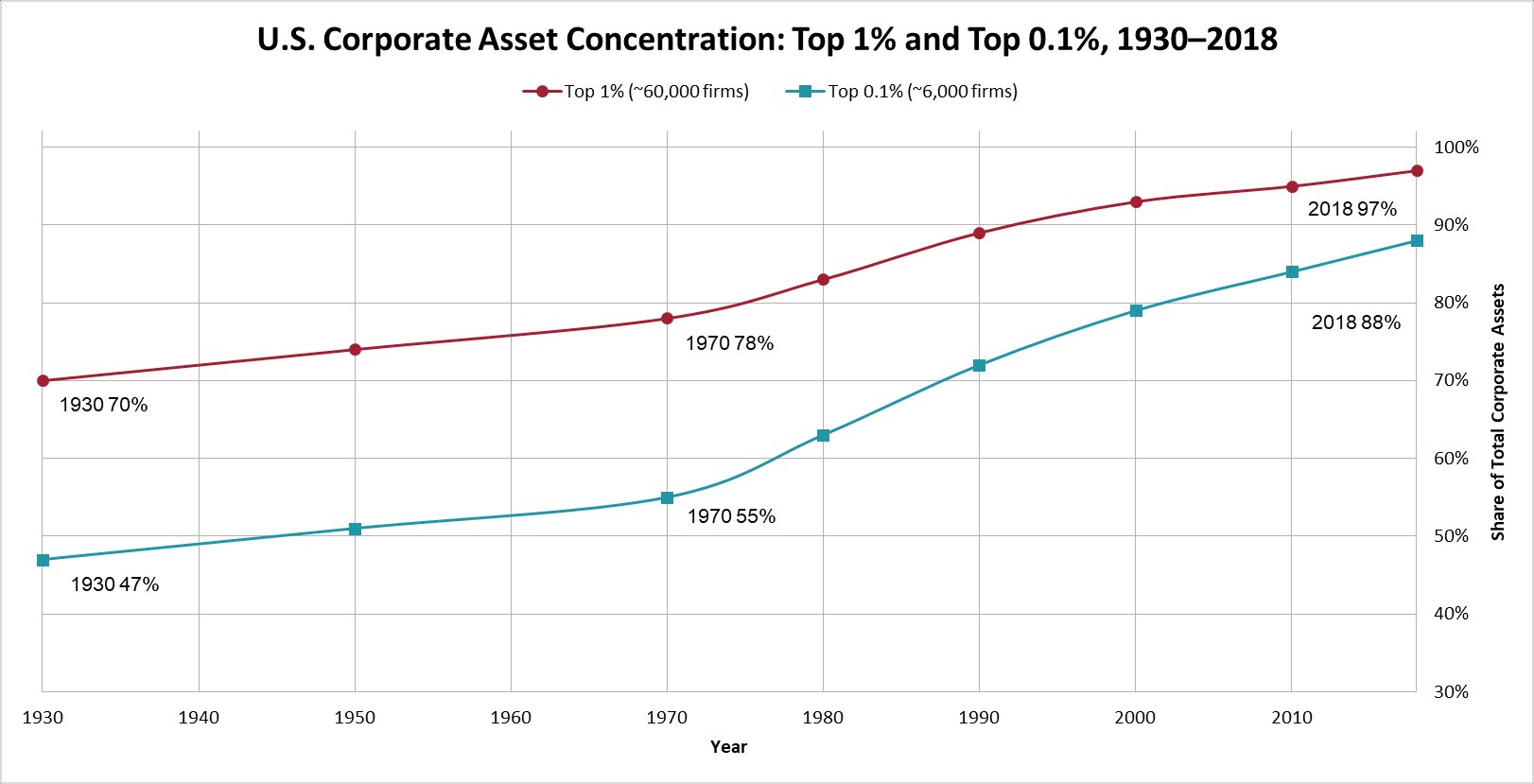

The U.S. economy has become increasingly concentrated and dominated by large, creditworthy companies, as illustrated in the charts below.

S&P 500 Market Capitalization vs. U.S. Nominal GDP, 1990–2024

S&P 500 Market Capitalization vs. U.S. Nominal GDP, 1990–2024 | Sources: Siblis Research / S&P; BEA Table 1.1.5 | Chart: CRE42

U.S. Corporate Asset Concentration: Top 1% and Top 0.1% of Firms, 1930–2018

U.S. Corporate Asset Concentration: Top 1% and Top 0.1% of Firms, 1930–2018 | Source: Kwon, Ma & Zimmermann, American Economic Review, July 2024 | Chart: CRE42

The S&P 500’s aggregate market capitalization stood at roughly 0.5 times U.S. nominal GDP in 1990; it first crossed GDP in 1997 and reached 1.5 times GDP by year-end 2024, with the index representing approximately $43.7 trillion in market value against $29.2 trillion in annual economic output.[8][9] At the firm level, peer-reviewed IRS data shows the asset share of the top 1% of U.S. corporations — approximately 60,000 firms out of roughly 6 million total corporate filers, the remaining 99% of which are predominantly small incorporated entities with minimal assets — rising from 70% in the early 1930s to 97% by 2018. The top 0.1%, approximately 6,000 firms, held 88% of all corporate assets by 2018, up from 47% in the early 1930s. Concentration in services, retail, and wholesale accelerated specifically after the 1970s.[10]

Corporate growth through consolidation has helped the NNN single-tenant asset class grow disproportionately to the overall retail landscape over the last two decades. Dollar General, for example, operated approximately 8,200 stores in 2007; by fiscal year 2024 it operated over 20,600, a 151% increase in store count over 17 years.[11] Each location is a freestanding NNN property under a long-term corporate guarantee. Across the discount, QSR, auto parts, and convenience sectors, similar national chain acquisition-led expansions have created a deep and liquid market for single-tenant investment-grade retail product that did not exist at the same scale in the early 2000s. See the accompanying data file for detailed information on the sub-sectors of NNN single-tenant retail.

Grocery-Anchored Neighborhood Centers

Grocery-anchored centers are the most durable format in the retail sector. The format predates the modern CRE industry; supermarket-anchored strips have existed in American suburbs since the 1950s. Grocery sales have not declined in a single year of the Census MRTS data series going back to 1992.[1] This structural resilience — food-at-home spending is non-cyclical and non-shippable in meaningful volume — insulated grocery-anchored centers from both the 2008 recession and the COVID-19 disruption that temporarily closed most enclosed retail. Aldi and Lidl, both expanding aggressively in the U.S., have added new anchor demand in markets previously considered saturated. New supply is negligible; no grocer builds into a trade area it already controls. Kimco Realty (KIM) and Regency Centers (REG), the two major public grocery-anchored REITs, have posted consistently high occupancy rates above 95% in recent years.

Unanchored Strips (Convenience and Service Retail)

Unanchored neighborhood strips — small-format centers occupied by daily-needs service tenants including urgent care, nail salons, quick-service restaurants, dry cleaners, and tutoring centers — existed as an asset class for decades before receiving institutional attention. The format was institutionalized in September 2024 when SITE Centers spun off Curbline Property Corp (CURB) as a standalone REIT specifically to hold convenience and service-oriented unanchored strips. The Curbline thesis holds that these tenants are e-commerce resistant (services cannot be digitized), generate the highest visit frequency of any retail format, and follow residential rooftop growth rather than anchored shopping patterns. Vacancy for this subtype is comparable to grocery-anchored and considerably tighter than power centers or malls.

Power Centers

Power centers — open-air centers anchored by large-format, category-dominant tenants — were the defining retail development format of the 1980s and 1990s. Home improvement, consumer electronics, sporting goods, and office supply chains drove the format’s proliferation. Centers anchored by durable tenants including Home Depot, Costco, TJX/Marshalls, Burlington, and fitness operators are stable and well-occupied, while centers dependent on the prior generation of big-box anchors carry significant vacancy. Sears, Kmart, JCPenney, Bed Bath & Beyond, Circuit City, Sports Authority, and similar chains vacated millions of square feet of anchor boxes during closures spanning 2005–2023. Those boxes are converting to mixed-use, self-storage, medical, and multifamily at varying rates depending on trade area demographics and zoning flexibility.

Lifestyle Centers

Lifestyle centers emerged in the mid-1990s as a response to enclosed mall fatigue. The format featured open-air, walkable design, premium landscaping, and soft-goods anchors — Apple Stores, Pottery Barn, Lululemon, Williams-Sonoma — rather than department stores or grocery chains. Development was concentrated in affluent suburbs from roughly 1995 to 2010; the format has not been meaningfully replicated since. Lifestyle centers benefited from the COVID-era shift to open-air retail and have generally maintained occupancy by migrating tenant mix toward food and beverage and experiential uses. Their primary vulnerability is sensitivity to discretionary spending: the “barbell consumer” phenomenon — spending concentrating at the luxury end and the value end while middle-market discretionary contracts — hits lifestyle centers harder than necessity-based formats. Performance correlates strongly with trade area household income.

Enclosed Malls

Enclosed malls are arguably the most analyzed retail format in commercial real estate. Aggregate vacancy figures for the sector are misleading because they blend two fundamentally different businesses. At peak the United States had approximately 2,500 enclosed malls; the count has contracted to roughly 1,000–1,350 depending on the classification threshold used, with continued attrition expected among the bottom tier.[6] The approximately 200–400 Class A malls — typically located in high-barrier, high-income trade areas with strong tourism or flagship tenancy — are performing well, with occupancy above 95% and in-line rents growing. Simon Property Group (SPG), concentrated in Class A assets, has reported consistent NOI growth. The bottom 700–900 Class B and Class C malls face anchor vacancies, declining foot traffic, covenant issues with surviving tenants, and active redevelopment or conversion pipelines. CBL & Associates and Washington Prime Group, both concentrated in lower-tier mall assets, filed for bankruptcy in 2020.

Urban / High Street Retail

Urban retail corridors predate every other format on this list and are the most heterogeneous category. Fifth Avenue, Rodeo Drive, Michigan Avenue, Newbury Street, and comparable corridors were institutionalized as investment categories in the 2000s as international luxury brands expanded U.S. flagship operations. Flagship luxury corridors in New York, Los Angeles, and Miami have recovered to or above pre-COVID rents, while second-tier urban corridors dependent on office worker foot traffic remain materially impaired and track office occupancy closely.[7] International luxury brands are consolidating to fewer, larger flagship doors rather than maintaining broad urban retail networks, which concentrates performance at top-tier corridors and amplifies distress elsewhere.

What to Watch in 2026

Sources to Track Retail Format Data:

| Source | Release | Frequency | Notes |

|---|---|---|---|

| Census Bureau MRTS | Monthly Retail Trade Survey | Monthly | Tenant-category sales data; tracks department stores, grocery, pharmacy, restaurants, e-commerce by NAICS code. |

| Colliers Retail Report | Quarterly U.S. Retail Market | Quarterly | Subtype-level vacancy breakdown including mall vs. shopping center vs. freestanding. |

| CoStar | Retail Subtype Analytics | Ongoing | Primary source for subtype-level vacancy, rent, absorption, and cap rate by MSA. Subscription required. |

| NAREIT | Monthly REIT Index Returns | Monthly | Shopping center vs. regional mall vs. freestanding total returns; tracks investor-level format divergence. |

Notes

[1] U.S. Census Bureau. Monthly Retail Trade Survey (MRTS), Annual Retail Sales by Kind of Business. census.gov/retail ↩

[2] Colliers International. U.S. Retail Market Report, Q4 2025. colliers.com ↩

[3] Cushman & Wakefield. U.S. Retail MarketBeat, Q4 2025. cushmanwakefield.com ↩

[4] CVS Health. CVS Health Announces Store Optimization Initiative. (2022). investors.cvshealth.com ↩

[5] Walgreens Boots Alliance. Walgreens Announces U.S. Store Footprint Optimization. (2024). investor.walgreens.com ↩

[6] ICSC Research. U.S. Mall Count and Classification. icsc.com/research ↩

[7] JLL. U.S. Retail Outlook, Q4 2025. us.jll.com ↩

[8] Siblis Research. S&P 500 Historical Market Capitalization. siblisresearch.com ↩

[9] U.S. Bureau of Economic Analysis. National Income and Product Accounts, Table 1.1.5: Gross Domestic Product. bea.gov ↩

[10] Kwon, S.Y., Ma, Y., & Zimmermann, K. 100 Years of Rising Corporate Concentration. American Economic Review, 114(7), 2111–2140. (July 2024). aeaweb.org ↩

[11] Dollar General Corporation. Annual Reports, 2007–2024. ir.dollargeneral.com ↩

Companion workbook. retail-format-divergence.xlsx — Underlying data for all charts (Census MRTS, 2000–2024; S&P 500 market cap vs. GDP; U.S. corporate concentration)

Methodology & Data Notes

Census MRTS: What Is and Is Not Measured

The Monthly Retail Trade Survey (MRTS) tracks sales by tenant category (NAICS code), not by retail property format. A department store sale is recorded under NAICS 4521 regardless of whether the store is located in an enclosed mall, a power center, or a freestanding building. Accordingly, MRTS data documents the collapse of the department store business category and the growth of the warehouse club and restaurant business categories, but does not directly measure building-type vacancy or rent.

Nominal vs. Real

All sales figures in the charts are nominal (not inflation-adjusted). In real terms, the decline of department stores and the growth of food service are even more pronounced. Grocery sales growth also overstates real volume growth due to food price inflation, particularly post-2020.

S&P 500 Market Capitalization Data

S&P 500 market capitalization figures are year-end values sourced from Siblis Research, which compiles historical S&P data from Standard & Poors filings. Siblis is a secondary aggregator; these figures are consistent with other published sources but are not a primary government data series. U.S. nominal GDP is from BEA Table 1.1.5, which is a primary government source. The S&P 500 represents approximately 80% of total U.S. equity market capitalization.

Corporate Concentration Data

The corporate asset concentration figures (top 1% and top 0.1%) are from Kwon, Ma & Zimmermann (2024), published in the American Economic Review. Endpoint values (early 1930s and 2018) are cited directly from the published abstract. Intermediate decadal values shown in the chart approximate the described persistent upward trend and are not individually cited data points. The terminal year of 2018 reflects the publication lag inherent to IRS Statistics of Income (SOI) administrative tax data, which the authors use as their primary source; SOI records at the level of detail required for this analysis typically carry a 5–6 year lag from data year to research publication. The denominator is all U.S. corporate tax filers, approximately 6 million entities annually, the vast majority of which are small incorporated entities (LLCs, holding companies, sole proprietors) with minimal assets. Full underlying data is available at businessconcentration.com.

Vacancy and Rent Data

Subtype-level vacancy and rent figures cited in Key Observations are sourced from Colliers, JLL, and Cushman & Wakefield Q4 2025 national reports. These brokerages define retail subtypes differently: Cushman & Wakefield shopping center vacancy excludes malls and freestanding; Colliers includes all subtypes. Direct averaging across sources is not performed where definitions diverge materially.

Share Calculation

Category shares in the bar chart are calculated as a percentage of total retail sales as reported in the MRTS, excluding motor vehicles and gasoline. Total retail (ex-auto, ex-gas): $2,915B in 2000; $7,265B in 2024. The denominator growth reflects both inflation and real volume expansion, which means categories with stable absolute sales show declining share.