Overview

Between January and April 2026, roughly $1 trillion of public software market capitalization was erased. The iShares Expanded Tech-Software ETF (IGV) was reported down approximately 28% year-to-date by mid-April and approximately 35% off its October 2025 high. The selloff was named the “SaaSpocalypse” by Jefferies equity trader Jeffrey Favuzza in late January and the term was picked up by Forbes, CNBC, and the Wall Street Journal in subsequent weeks.[1]

The trigger was not a single event but a sequence of Anthropic product releases that began with Claude Cowork on January 12, 2026 — an AI agent for non-developers capable of executing multi-step business workflows on a user’s desktop. The releases that followed (open-source plugins on January 30; Claude Opus 4.6 on February 4; Claude Managed Agents on April 9; Claude Design on April 17) compounded the original repricing. Each release prompted analysts to widen the set of software categories considered structurally exposed to AI-agent substitution.

For commercial real estate, the SaaSpocalypse matters less as a stock-market event and more as a leading indicator. The same AI capabilities that justify a 30% repricing of public SaaS equities — agents that read files, draft documents, run analyses, and complete multi-step business tasks — are the capabilities that, if deployed at scale by enterprise customers, would reduce demand for entry-level white-collar workers. Office demand in tech-heavy and professional-services-heavy metros (San Francisco, Seattle, Austin, parts of New York) is the most direct CRE channel for this risk. The repricing is a market signal that the displacement scenario described in the AI & Knowledge Work page has moved from possibility to probability in the eyes of equity investors.

Six-Month Stock Performance (Top 10 SaaS)

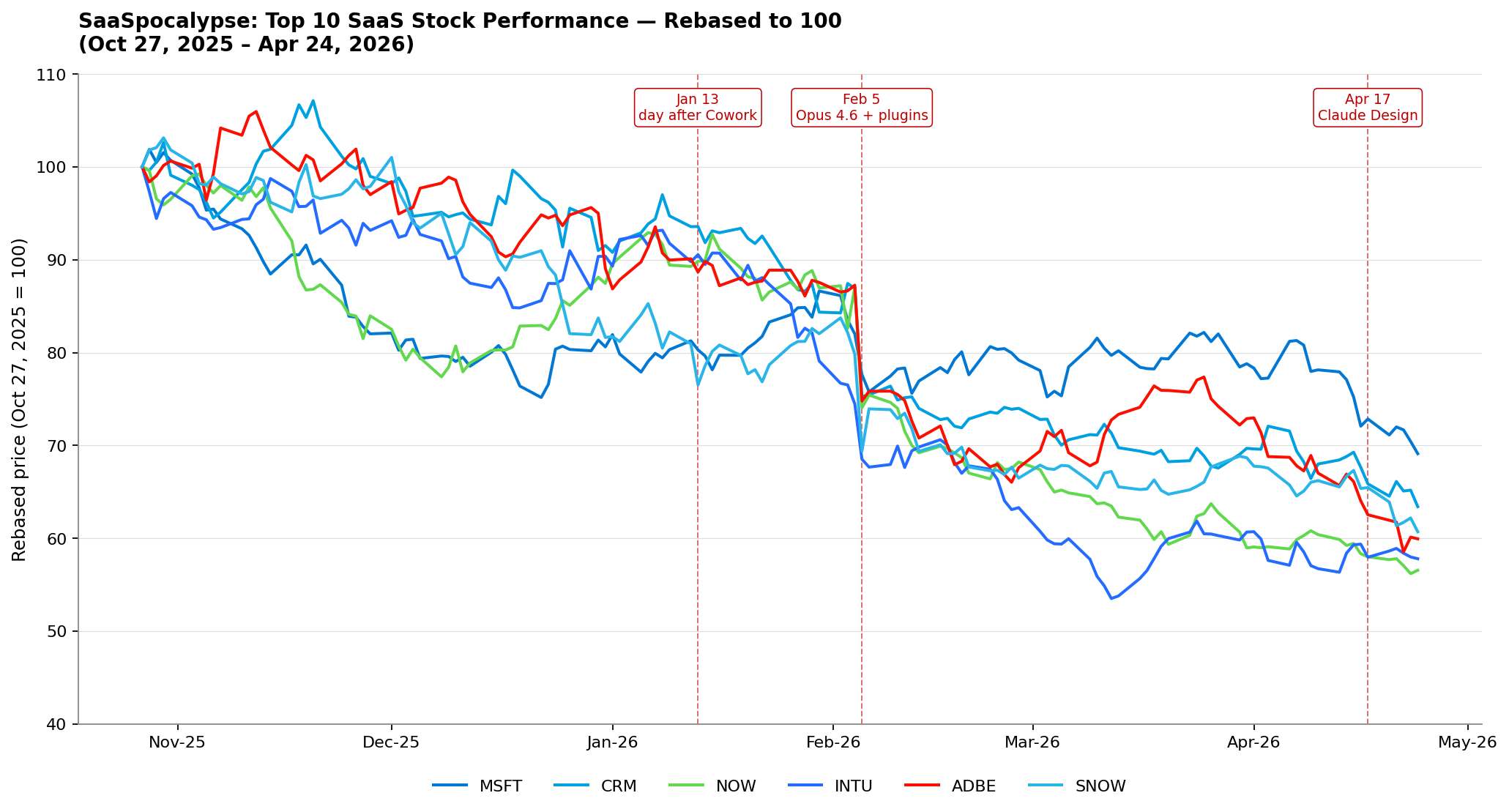

Top 10 SaaS Stock Performance, Rebased to 100 (Oct 27, 2025 – Apr 24, 2026) | Source: CRE42 analysis of daily closing prices for select SaaS-exposed equities. Top 10 universe by market capitalization includes three hybrid names (MSFT, ORCL, SAP) and seven pure-plays (CRM, NOW, INTU, ADBE, CRWD, PANW, SNOW). Six tickers shown for chart legibility.

The chart above shows six representative names from the Top 10. The single most striking feature is the February 5, 2026 cliff: every line drops between approximately 8% and 15% in a single trading session. That session combined the broader Cowork-plugin overhang from earlier in the week (the legal plugin had triggered a $285 billion rout in software, financial services, and asset-management stocks on February 3) with the announcement of Claude Opus 4.6, marketed by Anthropic as capable of orchestrating teams of AI agents and excelling at financial analysis, due-diligence research, and market-intelligence synthesis — functions priced into the valuations of incumbent SaaS data and analytics providers.[2]

Six-month total returns for the Top 10 averaged approximately -25%, with average drawdown from the period high of approximately -32%. Pure-play SaaS names took the worst of it: ServiceNow (-43%), Intuit (-42%), Adobe (-40%), Snowflake (-39%), and Salesforce (-37%). The hybrid names with broader business mixes were less affected (Oracle +8%, SAP -15%, Microsoft -31%). Cybersecurity names (CrowdStrike, Palo Alto Networks) were notably less affected (-3% and -5%), consistent with the analyst consensus that mission-critical security workloads carry more durable pricing power than horizontal productivity software.[3]

Key AI Announcements and Stock Reactions

The selloff unfolded as a sequence of distinct trigger events rather than a continuous decline. The table below records the most notable single-session moves where contemporaneous reporting tied the price action to a specific AI announcement. Day-of percentages are event-day close versus prior trading day’s close.

| Date | Event | Stock(s) | Move |

|---|---|---|---|

| Jan 12, 2026 | Anthropic launches Claude Cowork — agent for non-developers, executes multi-step business workflows | ORCL | −2.8% |

| Jan 13, 2026 | Day-after digestion; first full session after Cowork launch | SNOW −5.5%, CRWD −5.1% | see left |

| Jan 28, 2026 | CNBC’s Deirdre Bosa builds a Monday.com-style kanban interface using Cowork in under an hour; tweet goes viral | MNDY (per CNBC) | −6% intraday |

| Jan 30, 2026 | Anthropic releases 11 open-source Cowork plugins (legal, finance, marketing, sales, customer support) | CRM −3.5%, INTU −3.7% | see left |

| Feb 3, 2026 | Software ETF (IGV) −5.7% — worst session since April 2025; legal-plugin overhang per Bloomberg | Thomson Reuters, RELX, LegalZoom (per CNN) | TRI −15.8%, RELX −14%, LZ −19.7% |

| Feb 4–5, 2026 | Anthropic announces Claude Opus 4.6; Top 10 collapse on Feb 5 | NOW, ADBE, CRM, SNOW, INTU, MSFT | NOW −14.9%, ADBE −14.3%, CRM −13.4%, SNOW −13.1%, INTU −8.0%, MSFT −5.3% |

| Feb 9, 2026 | Monday.com Q4 earnings; management withdraws forward guidance citing AI uncertainty | MNDY (per CNBC) | −21% overnight |

| Apr 9, 2026 | Anthropic discloses $30 billion revenue run rate (up from $9 billion at end of 2025); releases Claude Managed Agents | MSFT, Cloudflare (NET, per 247 Wall Street) | MSFT −3.5%, NET −12% |

| Apr 14, 2026 | Anthropic CPO Mike Krieger resigns from Figma board; Claude Design rumors break | FIG, ADBE, WIX, GoDaddy (per OfficeChai) | FIG −6%, ADBE −2.7%, WIX −4.7%, GoDaddy −3% |

| Apr 17, 2026 | Anthropic launches Claude Design — powered by Claude Opus 4.7; generates prototypes, slides, mockups from prompts | FIG (per OfficeChai/Inbenta), ADBE, CRM | FIG −7.3% ($20.32→$18.84), ADBE −2.3%, CRM −2.6% |

The bear thesis behind the SaaSpocalypse is structural rather than cyclical. The enterprise SaaS pricing model that emerged in the 2010s charges per user (“per seat”) on the assumption that more humans using a tool generates more value. AI agents potentially break that assumption: a single agent can drive the seat instead of a human, and a single subscription to a foundation model can replicate functions that previously required separate seats in a CRM, an analytics tool, a project-management tool, and a document tool. Whether this displaces SaaS entirely or simply forces a repricing toward outcome-based or usage-based contracts is the central debate. Analysts who foresee continued SaaS dominance point to data gravity, compliance, audit, and integration costs that AI agents do not eliminate; analysts who foresee replacement point to the speed at which Anthropic, OpenAI, and Google have moved from chatbots to agentic workflows in roughly 18 months.

CRE Read-Through

Public-equity repricings are not the same as office demand declines, but they are useful leading indicators. The $1 trillion erased from SaaS market caps in early 2026 reflects an investor judgment that AI will reduce the headcount required to operate enterprise software-driven businesses — the same headcount that occupies office space, consumes urban professional services, and supports the apartment rental and retail markets in tech-concentrated metros.

The CRE channels are roughly:

- Office demand in tech-heavy metros — San Francisco Bay Area, Seattle, Austin, and the Boston Route 128 corridor have the highest concentrations of tech and professional-services employment. A tech-sector hiring slowdown driven by AI productivity gains would compound the existing post-COVID office vacancy problem in these markets. See Office Regional Divergence for the current state of regional office vacancy.

- Multifamily in tech-heavy metros — the same demographic of entry-level knowledge workers that the equity market is repricing out of the SaaS labor force is the marginal renter in expensive coastal markets. A reduction in 22–25-year-old hiring would compound the affordability gap discussion in Delayed Family Formation.

- Retail in tech-heavy metros — downstream effects on urban food, fitness, and discretionary retail in metros with high concentrations of well-paid knowledge workers.

- Data centers — The AI capacity that threatens incumbent SaaS valuations is built on the hyperscaler capex described in Data Center Capital Spending. Capital is migrating from one CRE category (office) to another (data centers).

What to Watch in 2026

| Indicator | Source | Frequency / Next Update |

|---|---|---|

| Software ETF performance (IGV, WisdomTree Cloud) | iShares IGV factsheet; WisdomTree WCLD | Daily |

| Anthropic revenue run rate & product announcements | anthropic.com/news | Continuous; major announcements every 4–8 weeks in 2026 |

| OpenAI enterprise product cadence | openai.com/news | Continuous |

| Salesforce, ServiceNow, Workday, Adobe earnings | Company investor relations sites & SEC filings | Quarterly; next major round late May 2026 (Q1 2026 fiscal results) |

| Anthropic Economic Index — AI usage by occupation | anthropic.com/economic-index | Quarterly; next expected ~Apr 2026 |

| Entry-level hiring in tech, finance, legal occupations | Stanford Digital Economy Lab / FRED via Indeed | Periodic; track 22–25 age cohort employment in AI-exposed fields |

| Tech-metro office vacancy & absorption | CoStar, JLL, CBRE quarterly office reports for SF, Seattle, Austin, Boston | Quarterly; next round: late Apr 2026 (Q1 2026) |

| SaaS M&A activity & private valuations | PitchBook; major brokerage M&A research | Quarterly; depressed public valuations are accelerating consolidation |

[1] The term “SaaSpocalypse” was coined by Jefferies equity trader Jeffrey Favuzza in late January 2026 and adopted by Forbes, TechCrunch, and the Wall Street Journal. IGV ETF performance figures are reported on iShares’ product pages and in CNBC coverage of the software selloff. ↩

[2] Anthropic announced Claude Opus 4.6 on February 4, 2026 and the broad SaaS dump occurred on February 5. The $285 billion legal-plugin rout figure is from Bloomberg coverage on February 4, 2026. Single-day percentages cited above are computed from daily closing price data tracked in the accompanying Excel workbook. ↩

[3] The cybersecurity outperformance argument was articulated by Rolf Bulk of Futurum Group in CNBC coverage on February 6, 2026: “a subset of software providers, especially those running mission-critical enterprise workloads such as Oracle and ServiceNow, still have a sustained right to earn.” ↩

Document Links

technology-saaspocalypse.xlsx — Six months of daily closing prices for the Top 10 SaaS companies (Oct 27, 2025 – Apr 24, 2026), formula-driven performance summary with returns and drawdowns, embedded multi-line stock chart with event annotations, and a chronological table of 18 AI announcement-related stock reactions with sources.

Sources

[1] CNN Business, “Anthropic’s new AI tool sends shudders through software stocks” (Feb 4, 2026). cnn.com

[2] CNBC, “AI fears pummel software stocks: Is it ‘illogical’ panic or a SaaS apocalypse?” (Feb 6, 2026). cnbc.com

[3] CNBC, “AI threat’s relentless flogging of software stocks shows no end in sight” (Apr 9, 2026). cnbc.com

[4] Fortune, “Anthropic’s Claude triggered a trillion-dollar selloff. A new upgrade could make things worse” (Feb 6, 2026). fortune.com

[5] CNBC, “Monday.com drops 21% as AI disruption fears mount in software” (Feb 9, 2026). cnbc.com

[6] Gizmodo, “Anthropic Launches Claude Design, Figma Stock Immediately Nosedives” (Apr 17, 2026). gizmodo.com

[7] OfficeChai, “Figma’s Stock Falls 7% After Anthropic Introduces Claude Design” (Apr 17, 2026). officechai.com

[8] Salesforce Ben, “Salesforce Stock Slides Further as AI Pummels ‘Dying’ SaaS Market” (Feb 25, 2026). salesforceben.com

[9] Daily closing price data for the Top 10 SaaS companies are tracked in the accompanying Excel workbook (link above). Universe and methodology are documented on the workbook’s README tab.